What Is Closing?

The Final Step to Ownership

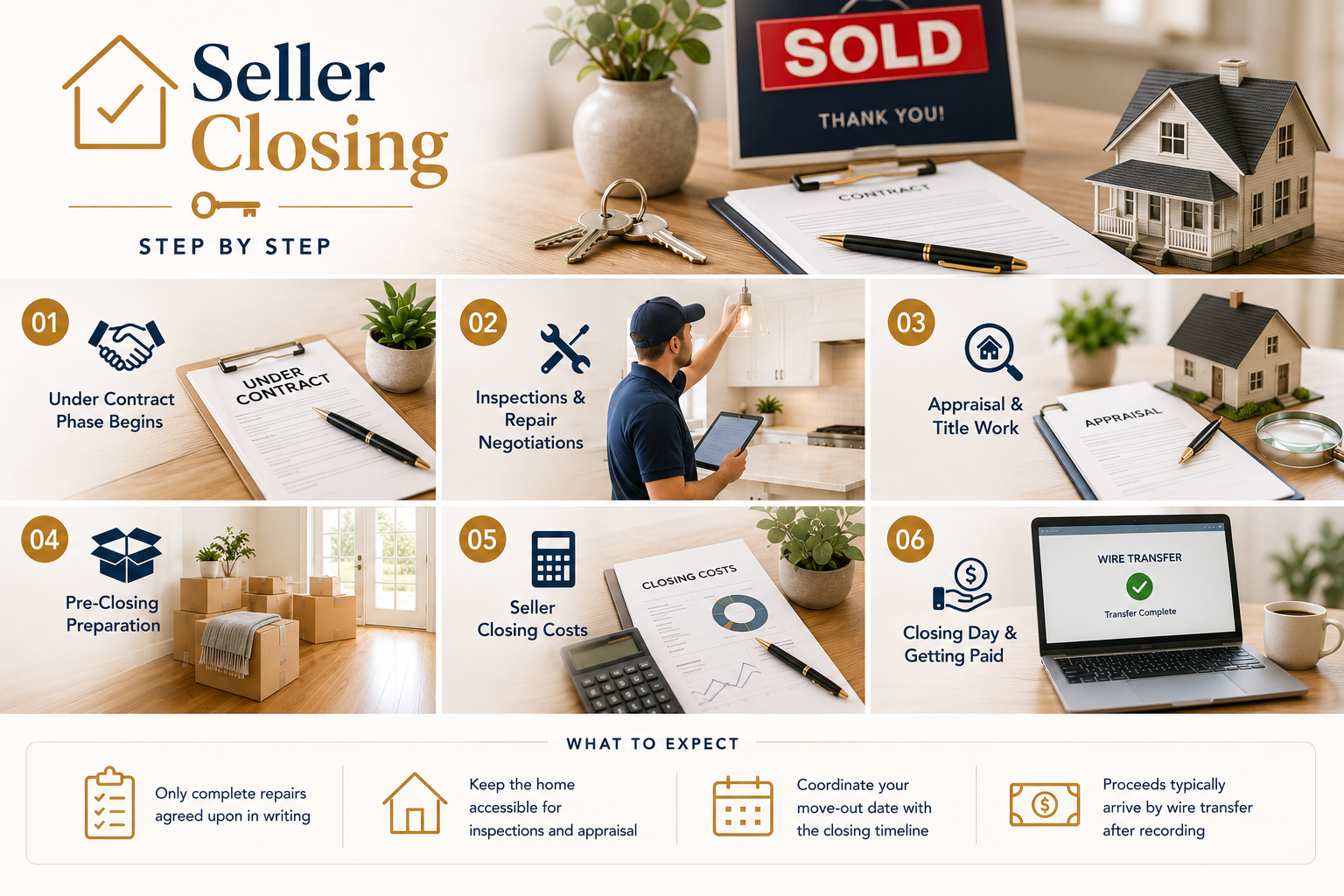

Closing is the final legal step that transfers ownership of a home from the seller to the buyer. It involves signing documents, transferring funds, and recording the deed. Understanding every step — whether you’re buying or selling — helps you move through the process with confidence and no unexpected surprises.

30–45

Days avg. buyer closing

30–60

Days avg. seller closing

2–5%

Typical closing costs

~12

Steps from offer to keys